When Should You Start Investing For Your Child’s Education?

The answer is As soon as possible.

Remember, Farhan Qureshi of the 3 Idiots movie? His father, Mr. Qureshi wanted him to become an engineer and he even started planning from the day his son was born. Though we don’t want to discuss the senior’s Qureshi career choice, i.e.; engineering and Farhan’s passion, i.e., wildlife photography, we want to draw your attention towards the need of starting investing early for your child’s education.

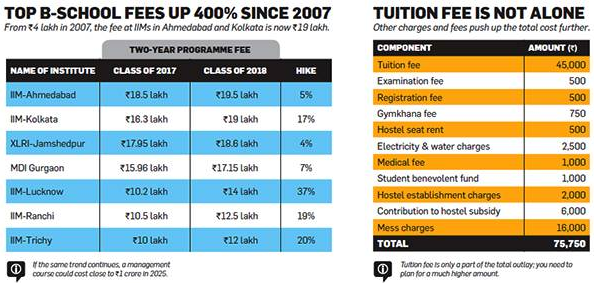

Though, giving a good education to a child is the dream of most of the parents, sadly, it is also one of the ‘expensive dreams’.

A price to be paid for ‘learning’

Source: The Economic Times

For most of us, these are big numbers and look like intimidating goals to accomplish. Undoubtedly, your earning will rise over the years, so will your expenses also. Your money should work as hard as you do to help you reach your financial goals.

Here are some of the reasons why you should invest early:

- Compound interest creates magic:

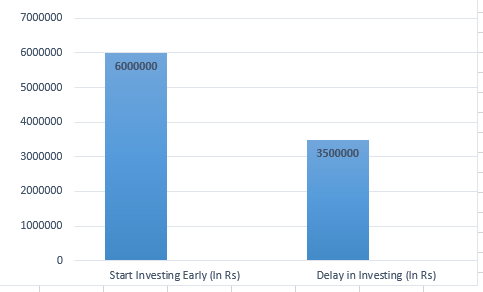

Taking the above discussion forward, the right time to start planning for your child’s education is from the day your little angel comes into your life. If you begin saving for day 1, you would have to save a smaller amount to accomplish your financial goal as the power of compounding will get enough to show its magic.

As said by Albert Einstein, “Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.

”The basic principle of compound interest is that you will earn interest even on the interest earned. The benefit of compounding works better over the time. It means, the longer the tenure of your investment, more money you will be able to accumulate due to the compounding effect. So, when you start investing early, the time is at your stride, and it means, you can accumulate more money than the person who postpones his/her investment plans.

For instance, if you start investing Rs 10,000 monthly from today for 20 years, you will get Rs 60 lakh (approx.) after 20 years, considering the rate of return as 8%. If you delay your investment by five years, you will be able to accumulate approximately Rs 35 lakh (approx.). There is a clear difference of Rs 15 lakh (32-28).

Here, the early bird catches the worm is an idiom worth adhering to. Even if at some point in time, your finances become unstable, by investing early, you’ll be able to offset its adverse impact. An early start can save you from the heartaches later in life.

Here, the early bird catches the worm is an idiom worth adhering to. Even if at some point in time, your finances become unstable, by investing early, you’ll be able to offset its adverse impact. An early start can save you from the heartaches later in life. - More time to take risks

We human beings have the tendency to commit mistakes. The same happens with investment also as not all of us get our investment options correct the first time. When you start investing for your child early in your life, you would have a greater ability to take risks in comparison to a person who has not started yet. This is because, at a later stage in your life, when your goal is only a few years away, you will be extra cautious with your choice of investment. Also, you will have limited investment options available to you.Those who begin to invest early have more time to recover if something goes wrong. - Money available when you need it most

When you invest early, you would have a comfortable cushion backing you up. It means, you can rest assured that your savings will be there to help you when you need it most.

Now where to invest?

As time is on your side, equity funds should be your preferred choice of investment option for you. Though, many people afraid of investing in equity, considering it as a risky option, the volatility of returns will be flattened out in the long run. Moreover, child insurance plans offered by insurers like ICICI Prudential allow you to invest a portion of your funds in equity and debt as per your risk appetite, which you can also switch as per the market conditions.

A child ULIP insurance plan comes with a dual benefit of life cover and sum assured. Like an investment, it will grow your money and in case anything happens to you, the life cover will be paid which can be used to meet immediate expenses, like child’s education fees, household expenses etc. Also, the insurer will waive off future premiums but the policy will continue till maturity.

In addition to child ULIPs, one can also invest in stocks, balanced & debt funds, monthly income plans of mutual funds, recurring deposits, short-term debt funds, gold, etc.; to reap more benefits.

Conclusion

The foundation of future lies today, so smart moves make by you today, will frame your child’s tomorrow. And that is what every loving parent, like you, want, isn’t it?

Plan for your child’s future ‘now’ to avoid scrambling around at the last minute to find ways to finance your loved ones’ education or worse, compromising on the quality of education, simply because you can’t afford it.

So, reiterating what we said earlier, the best time to start investing for your child is NOW.